Am I the only one in HN who is not into the stock market? I live in Western Europe and I would say 75% of my acquaintances don't do stock market. People I have known in the past (old people) didn't do stock market either. They all seem to have lived a normal life (decent jobs, decent house, decent family). Nothing extravagant but they got enough money to be "happy" in life.

Europeans can have the luxury of not worrying about investing since many European countries offer livable pensions (for now…the demographic future for this isn’t looking so good).

However, this isn’t as great as it sounds. While the European model for healthcare and education is better, their pension schemes are arguably a much worse deal than what Americans can have.

In Europe, you’re basically paying the government to take your money and invest it in much too conservative, in fact, negative-yielding! bonds right now due to pension fund mandates.

You can’t take the proper amount of risk given your age (in your 20s-40s you should be almost fully allocated to stocks) because the pension fund needs to constantly be paying out money to old people—they can’t risk huge drawdowns.

There’s a surprisingly large amount of middle class Americans who will retire millionaires just because they are able to save for their pension privately and take the proper amount of risk for their age (eg. Target date funds).

Meanwhile, in Europe, governments shelter people from the harsh realities of how financial markets work, but you have to hope and pray that enough people are born in the coming decades to make up for the conservative pension mandates. And you have to pray that the government allows you to retire sometime before you die (in the nordics, retirement ages are constantly being pushed back and pension benefits are shrinking...due to said demographics).

I predict every country will eventually move to a hybrid private/public pension model like the US over the next 40 years. So you'll have to start caring eventually.

> a hybrid private/public pension model like the US

I'm not sure pensions exist in the US beyond a few public sector ones. The US model is entirely private at this point for all intents and purposes.

Also keep in mind that only about 55% of the US population owns any stock (including retirement accounts) [0], so (IMO, not an economist) the US is most likely looking at a retirement crisis in the coming decades.

The US has a public pension scheme called "social security," which guarantees at least a minimum level of income in retirement to all citizens (although, not enough to live on IMO).

This is intended to be supplemented with private investments via 401k & IRAs, which are actually relatively new programs (created in the late-1970s, but nobody even talked much about them until the 90s).

So while most millennials understand they need to be saving privately in these vehicles (r/personalfinance has 15 million members), there's a huge forgotten generation in the middle who slipped through the cracks between the transition from industrial-era corporate pensions to personal saving.

These are the folks who will unfortunately bear the brunt of the retirement crisis, having to get by only on Social security.

This is a myth. People struggle on state pensions throughout Europe, but for some reason young Americans idealize everything that comes out of Europe.

In Germany(a country of 80 mil), the average pension is $1000 once you get to 65. In France it's not much more. The social security in the US beats that, plus you can usually afford a private pension, because the government doesn't take 50% of your paychecks.

I personally know someone in Austria that worked all his life for the railroad, then he got sicker and sicker, but the state wouldn't give him a disability pension. He could barely work sitting all day. Then he got disability at around age 60, but he needed money so much that he had to collect scrap metal to make ends meet. Very sick, after 60 years old, collecting metal. This is just an anecdote...I know, but still.

In France, the average pension is 1393€ (~ $1574) [1]

Also the retirees purchasing power is higher than the working population [2]

Don't get me wrong, there are still too many retirees with too little money in France.

But on average, the retirees are doing OK compared to the rest of the population.

I was commenting for the Americans. In the US you get a "meagre" state pension (social security) and people believe that Europeans have so much more...well that US state pension is on average $1500. But Americans have in general much better private funds, because they have lower taxes.

It's absolutely true and Americans like to do the evangelization of these strange beliefs about Europe.

There are good and bad parts about every system and thinking everything is perfect in Europe is about as dumb as Euros are socialists and its bad dogma.

> There’s a surprisingly large amount of middle class Americans who will retire millionaires

This seems like a serious bug in the system, doesn't it? Why would old people retire as millionaries while young people struggle working long hours and can barely save anything?

Compounding interest...if you start early enough and take advantage of employer contribution matching, etc. But most people in the US won't retire as millionaires, let alone even retire. Unforeseen life events often cause people to dip into retirement savings and in some cases wipe out any gains. Also, once in retirement, life in the US can still be quite expensive. For example, Medicare and all the additional supplemental insurance(s) you need is absurdly expensive for retirees. Everything in the US is "out of pocket".

Because the lack of effective pensions require you to either work til you die or live off Social Security. Most people don't want to do either, so they direct a significant amount of their earnings to 401ks and the stock market.

The fact that young people struggle really doesn't have much to do with this.

In the UK you can stick whatever you want into stocks and shares isas, if you can afford it.

The problem is that housing costs rise to suck every spare penny of income from pretty much everyone so very few people have spare money to put into those isas.

I believe this is also a side-effect of these poor pension schemes.

European governments see the demographic timebomb coming, so they massively incentivize their citizens to invest in a primary residence, treating it as forced savings. This inflates local real estate values to ridiculous levels, especially while interest rates are low.

However, incentivizing your citizens to take leveraged bets (big mortgages) on a single piece of real estate is...not great.

This means the investment portfolio of the average European citizen is ONE specific apartment (zero diversification), and negative yielding sovereign bonds (via government pension funds).

Since most European mortgages are not fixed rate, it will be interesting to see what happens as interest rates start rising in Europe.

While the bonds will start paying better interest, that mortgage exposure might start to wreak havoc on the average citizens finances...

"Since most European mortgages are not fixed rate, it will be interesting to see what happens as interest rates start rising in Europe."

It's the second time I see this on HN. However, the reality seems more contrasted. From [1]:

"A striking feature of the credit market in the euro area is the very large heterogeneity across

countries in the granting of fixed versus adjustable rate mortgages. Fixed rate mortgages

(FRMs) are dominant in Belgium, France, Germany and the Netherlands, while adjustable

rate mortgages (ARMs) are prevailing in Austria, Greece, Italy, Portugal and Spain."

Something I didn't realise until recently was in the US it's normal to have a 30 year mortgage with a fixed rate from the start, rather than a fixed rate for a few years and then either a variable rate or requiring a remortgage. My understanding is that most mortgages in the Netherlands tend to be 5-10 years fixed rather than lifetime.

In the UK I feel there's a lot of distrust of stock markets amongst normal people, partly because the FTSE doesn't grow (back in 2000 it was about 7,000, today it's about 7,500), and that's the one reported on the normal news. There's no widely reported "FTSE dividend reinvested" measure.

Add in the mortgage mess from annuity mortgages where people were sold the idea they could have their cake and eat it too, ended up without enough money to repay their mortgage at the end. Throw in the pension collapse of Equitable Life, the pension fraud from Maxwell, the stock "boom" in the 90s where normal people bought shares, driven by the selloff of nationalised industries, and then seeing those shares vanish in 2000 and never really recovering and you get a general distrust of private hands managing money, and a preference to trust the government.

This meant people put their money into houses starting in the late 90s, which combined with increasing household income as new families became dual-income led to increasing house prices and a snowball effect. Even 2008 didn't really impact, as it was mainly sold as a US problem which had an effect on the UK, but not a major one.

The UK government (any colour) will do anything to keep house prices growing as that's how you get votes.

At least in the Nordics, most folks I know in the past years have been taking out floating rate mortgages.

Makes complete sense given interest rates are zero right now. However, if the ECB keeps getting surprised by inflation (like the Fed is in the US), interest rates may have to be start rising in fast, dramatic fashion.

Yes, for perspective relatively modest 3 bedroom houses in London are going up in price, every month, by more than the average person in the UK as a whole takes home.

You can be in the top 1% by income in London and still simply not be able to afford a small family home.

All the income from people in London is extracted by those owning the land, because you need to live somewhere to earn that money. It's basically monopoly, doesn't matter if you pass go and collect £200 or £2000, all that happens is the people owning the properties around the board take it until you run out (or if they want to extend the game

I am very worried (UK) that the government retirement safety net may not be there for us, as the retirement age is being pushed up beyond 70 but I am not sure most people can work full time that long without health issues.

Nor can we assume that the exceptional stock market returns of the past 15 years will be repeated, which means we need to save more for the same result.

I feel great pressure to earn a high wage in order to save a lot of it into a pension. This feel like a matter of survival.

Germany is even worse than you describe. The pension system managed by the government is not backed by any assets at all, but works by taking from the working population to the retired population. Given the age distribution in Germany this means young people are increasingly paying more to this system, while retired people receive less and less per person.

This was of course obvious already a while back, so the government decided to introduce additional ways to encourage saving for retirement (by giving tax discounts). However, they also managed to screw this up, because only contracts from certain insurance companies apply for these tax discounts. And these contracts have such a high management fee, that the real return of those constructs is negative.

<There’s a surprisingly large amount of middle class Americans who will retire millionaires just because they are able to save for their pension privately and take the proper amount of risk for their age (eg. Target date funds).>

Yet there's a surprisingly large amount of middle class Americans who have no retirement savings; either due to YOLO, or medical emergencies, or misunderstanding how to invest towards retirements.

It might depend on your definition of "surprisingly." According to this source, about 10% of American households are millionaires and about 80% of those are first-generation millionaires (i.e. they didn't inherit the money).

Additionally, only about 1% of those millionaires are under 35. (This is a point that gets lost in the debate about inequality, in my view; most wealthy people are old for what I think are extremely obvious reasons.)

In the UK almost everyone will have been moved over to a "defined contribution" pension whose value is determined by the stock market, usually in the form of a "stakeholder pension".

I don't "do" the stock market but I do have such a pension. And every few months sweep spare cash out of my current account into an index fund. Effectively I pay people to worry about this stuff on my behalf.

People who retired more than about 10 years ago are far more likely to have "defined benefit" pensions whose value is independent of the stock market.

Not the parent, but I live in Germany and while the new coalition government is expected to push for moving he public pension system to stock based pensions, the current system consists of a public pension system (that employees pay into via their employer to pay out current recipients who previously paid into it) and a private pension system everyone is strongly encouraged to pay into. As I understand it the private system is not directly tied to the stock market though.

For most people outside the very niche finance and tech investment bubbles stocks are largely understood as a form of gambling and managed funds as a high yield alternative to a savings account with a small risk of losing money (but this requires some disposable income so again this is somewhat self-selecting).

The ordinary Hans Wurst (German Joe Blow) just follows the economy section of the news for a general feeling of if things are going good or bad because line goes down means prices go up and they probably won't get a raise.

From a leftist point of view the most frustrating thing about red-green is that they market themselves as progressives and leftists but then just follow the same neoliberal economical politics as everyone else. It's deeply ironic that the reforms that did away with large swathes of the welfare state and labor protections were implemented by a red-green coalition government, not conservatives or the FDP.

The lesson most voters take away from this seems to be that leftism is just false advertising and if you vote for leftists you just get the same politics but more dishonest, not that the "leftists" they keep voting for aren't actually interested in leftist politics (though I can see why Die Linke might be unappealing as they're a headache even if you see them as the only viable option).

Everyone is exposed to it if they trade in the major currencies. The government will reduce the purchasing power of the currency to ensure the nominal returns to meet the defined benefit obligations are met. This, in turn, will boost the price of equities such as land and stocks, and eventually trickle down as inflation for food and fuel.

You will get your defined benefit pension, but how much you can buy with it is variable. And it is going to be less than you think. That is the only way the equation balances with lower economic growth (especially due to lower population growth) and increased competition for resources from the other 7B people in the world.

Whether or not you care about the stock market is basically a question of whether you run a functioning business or not. If you run a function business then you are have cash sitting on accounts. Even for a fairly modest business, a reasonable operating cushion dictates that you always have 6-7 figure cash reserve. Ideally you want this money to be sitting somewhere where it generates good returns, yet can be accessed quickly and with low transaction costs. Therefore shares and funds start to make sense. These days you can actually move cash directly into funds from your corporate online bank.

Shares (and all their financial derivatives) are a good hedge for profitable limited companies, because they either go up in value (yay! profit!) or down in value (yay! tax deductable loss rolled over to next year!). So long as the company is otherwise making a profit, shares are actually pretty hard to lose out on.

Also pensions. Most pensions are backed by index funds which are generally related somehow to stocks and shares. If you need to manage a pension fund, you have to pay at least vague attention to the stock market.

The stock market is a terrible - criminally negligent - place to keep a company's operating cash. I would be fascinated to read advice from an accountant or other financial professional that says otherwise.

I once worked at a company which used a money market fund for its cash. That gave them a slightly better return than a bank account. In the end, not sufficiently better to be worth bothering with.

If the company has an excess of cash and nothing good to spend it on, I think it's fine to put it in the stock market. Maybe you wouldn't count this as "operating reserves" - I wouldn't do that with the money that's earmarked to pay suppliers but not due for another month, but I would do it with the money that's earmarked for opening a new business location at an indefinite time in the future.

You can get whatever risk profile you want from the stock market in return for less yield. If you can accept two-nines certainty that you won't lose half your money in six months, any broad index fund will do. That would be acceptable for a lot of "modest businesses" which find themselves with "6-7 figures cash reserves". If you need better, you can do fancy things with options, or put a fraction of the money in the bank and invest the rest.

(I am a financial professional, but not in this field, and this is not financial advice)

Doesn't seem sensible to invest your operating cushion in something as volatile as the stock market, especially given the corralation between a recession causing your operating margin to crash and a recession causing your business to need that operating margin

The US stock market has been ridiculously pumped from the last decade-plus of money printing, I wonder how many people think that's normal.

Hedge your risk. Investors get diversity (portfolio) spacially: they get a piece of lots of businesses. Entrepreneurs diversify temporally: they can reasonably only put their time into one thing at a time, and only a few over a lifetime.

So if your business is doing well you can avoid putting all your eggs in one basket by investing some cash personally outside the business. And the easiest way is to jus put it into an index fund and then concentrate on your business.

Eggs and baskets. If I owned a company that provided for my current income, I would not want to place myself in a position where the faltering of that business killed both my current income and my retirement at the same time.

By all means plow a lot of it back into the business, but there’s good reason to pull some out over time as well.

You don't have to be "into" the stock market i.e. doing day trading. That's unlikely to make you rich unless you do it as a full-time job (and even then...). You can get lucky, but that's usually about it.

Instead, invest a regular amount of money monthly into ETFs. Those are relatively low-risk, but should still yield significant returns over the course of decades.

It's true that most people (at least in Germany) don't trust the stock market. The problem is that your wealth is being eaten up by inflation and interests on savings are low or even negative. You will lose money. In addition, Germany's mandatory pension funds are in a bad shape and most private insurances (e.g. Riester) are not worth it.

The situation is not the same as in my parents' generation and unfortunately, a lot of people are not realising that.

As a Swede in Switzerland, I think the main difference to the US is the cost. European commissions is mostly "buy and never look again." That fosters a culture where only a few people care and talk about it.

In Switzerland, I have to pay ~0.1% stamp duty on every purchase and sale of stocks and ETFs (in a Swiss broker). The UK has a 0.5% stamp duty on stocks. The idea for these brokers to compete on price doesn't make much sense at that point. It's "fine" that the normal fund has a 0.5-1% fee. There's some movement here, but only if you care to engage outside your existing bank (IBKR in the UK, Avanza++ in Scandinavia, Degiro in Europe in general).

Investing is good, and---as has been said---pensions are often invested in the stock market, whether you know it or not. But you just don't talk about it, because being active is costly. In Sweden, the defined contributions are auto-invested in a balanced fund unless you engage. There's something to be said about having sane defaults when you create a system.

As for the US, I'm not sure Robinhood was a step in the right direction. We should encourage people to own companies, not try to profit from Brownian motion. But that's perhaps a topic for another discussion.

Finally, I'm heavily into the stock market. I have several accounts across the world (though not really by design). I'm fascinated about this oddity that I can buy more food in the future just by having a different piece of paper, compared to someone else. But I also spend a stupid amount of time trying to find ways to reduce cost of investments. My guess is that most people don't, and it's kind-of the first step for a European that's paying >1% in fund fees. Or who don't even know how much they're paying.

There is a lot of interest in the stock market currently. Individual investors (‘retail’) have been buying a lot of stocks in the last 12 months.

Some would say this is typical behaviour before a crash. Business people become folk heroes (Musk) and the news is all about stocks and macroeconomics.

It is also the case that professional traders make a lot of money out of retail investors. The percentage of retail investors that actually make money are, iirc, quite small. It doesn't make sense to do something when you don't have the time to get good at it, and being bad at it means you're going to lose money.

Sometimes you're forced to (when an investment is tied into a basic necessity, like a house), but you're always going to be at a disadvantage.

I mean the rights of tenants are such that if you want to live in decent conditions / a stable domicile, you have to buy a house, thus becoming a property investor.

I think the act of buying a house to live in should be considered more an act of consumption than of investment.

It’s not 100% consumption, but it’s almost surely we’ll over 50% consumption and yet people get confused by the fact that a slice of it is forced savings and a sliver of it is an investment and they focus on these latter two more than is appropriate and in so doing are prone to less rational decisions than if they thought of it as mostly consumption IMO.

I think houses mostly do depreciate in value. The land underneath them does not and this can often mask the former.

I live in a nice part of my city. My house is 100 years old, has terrible insulation, very old retrofit wiring, and needs constant maintenance to stave off decline. The house, with all the upgrades over the years, is likely worth about what it was when built. The land underneath it is a lot more valuable than it was 100, or even 25, years ago.

Seems like semantics to me: you can't buy a house without essentially buying land. If you could, I absolutely would.

The fundamental problem here is not one of economics, but of politics. You can't live in a stable, dignified manner without paying to be part of a state-run monopoly (land ownership), so everybody who can does, so land titles (note the word) become absurdly expensive.

There is no real connection between land and living space - multiple story housing exists, and if housing was built to a reasonable density, there's more than enough land for everybody to live in whatever size house they could afford to build.

It’s sensible though to think “Why don’t houses depreciate like used cars? After all, they also wear out.”

Side note 1: There are places where you can (sometimes only can) lease the land for 99 years. This has the predictable effect in terms of willingness to build/improve the land, especially as the lease term is drawing to an end.

Side note 2: these discussions almost inevitably summon the proponents of land-value-tax to encourage denser use of valuable land. They’ll be along shortly, I’m sure.

> There is no real connection between land and living space - multiple story housing exists, and if housing was built to a reasonable density, there's more than enough land for everybody to live in whatever size house they could afford to build.

All land does not have the same or even similar perceived utility to all people. Some land is has much more demand relative to supply than other land.

Kitchens also don't appreciate in value. However, if you're trying to rent a flat in berlin, you'll probably find yourself paying brand-new+ prices for the previous tenant's kitchen.

I live in Germany and its the same. Not that that's a good thing. People here are old-fashioned and still believe in "Concrete gold."

Fact is, as soon as you've got a meaningful amount of wealth, you're going to want to invest it so you can either get income from it or grow the principal. It could be in a home, multiple properties, or the stock market.

> People I have known in the past (old people) didn't do stock market either. They all seem to have lived a normal life (decent jobs, decent house, decent family). Nothing extravagant but they got enough money to be "happy" in life.

No offense but you're going to have a tough time comparing to a boomer in terms of wealth generation and building if you're a millenial. I know people who got houses handed to them for very cheap 30-40 years ago, and those houses are worth tremendous amounts of money now. On top of that they have good pensions and insurance from a long time ago. Or they have a rental contract where they're paying 1/3rd of their neighbors so their expenses are low.

There's a great income and wealth divide in Europe between the haves and the have nots, and the haves are very good at keeping their wealth and passing it down to their heirs. Meanwhile in most European countries, punitive taxation makes it extremely difficult to move up in social class, even from middle class to upper middle class.

> Meanwhile in most European countries, punitive taxation makes it extremely difficult to move up in social class, even from middle class to upper middle class.

German has extremely liberal inheritance taxes. On the one hand this is often justified with the existence of the German "Mittelstand" (medium sized businesses typically owned by one family over generations), on the other this means the easiest way to get rich is to have rich parents.

Low inheritance taxes are actually a great predictor for maintaining social inequality over generations. If you wanted to reduce social inequality you'd instead want to drastically lower VAT (which disproportionately affects poorer people), adjust income taxes to lower the tax burden on lower incomes and raise it on higher incomes, and drastically raise taxes on income from capital (rather than labor). This isn't even simply an opinion, this is scientific consensus.

That reduces social inequality, but that is not the singular goal of a society. Producing goods and services and wealth for the nation is a goal that competes with “tax away almost all the gains of these activities”, which is why there’s debate about how to balance these things.

Frankly, who is "the nation" if not its people? As long as even a single individual suffers poverty, "the nation" has failed. If "the nation" is its people, protecting every single person from hardship is a higher goal than allowing a minority to live in excessive luxury.

If you think the "wealth of a nation" is measured by the luxury of a few rather than the poverty of the many, you might as well just revert to feudalism.

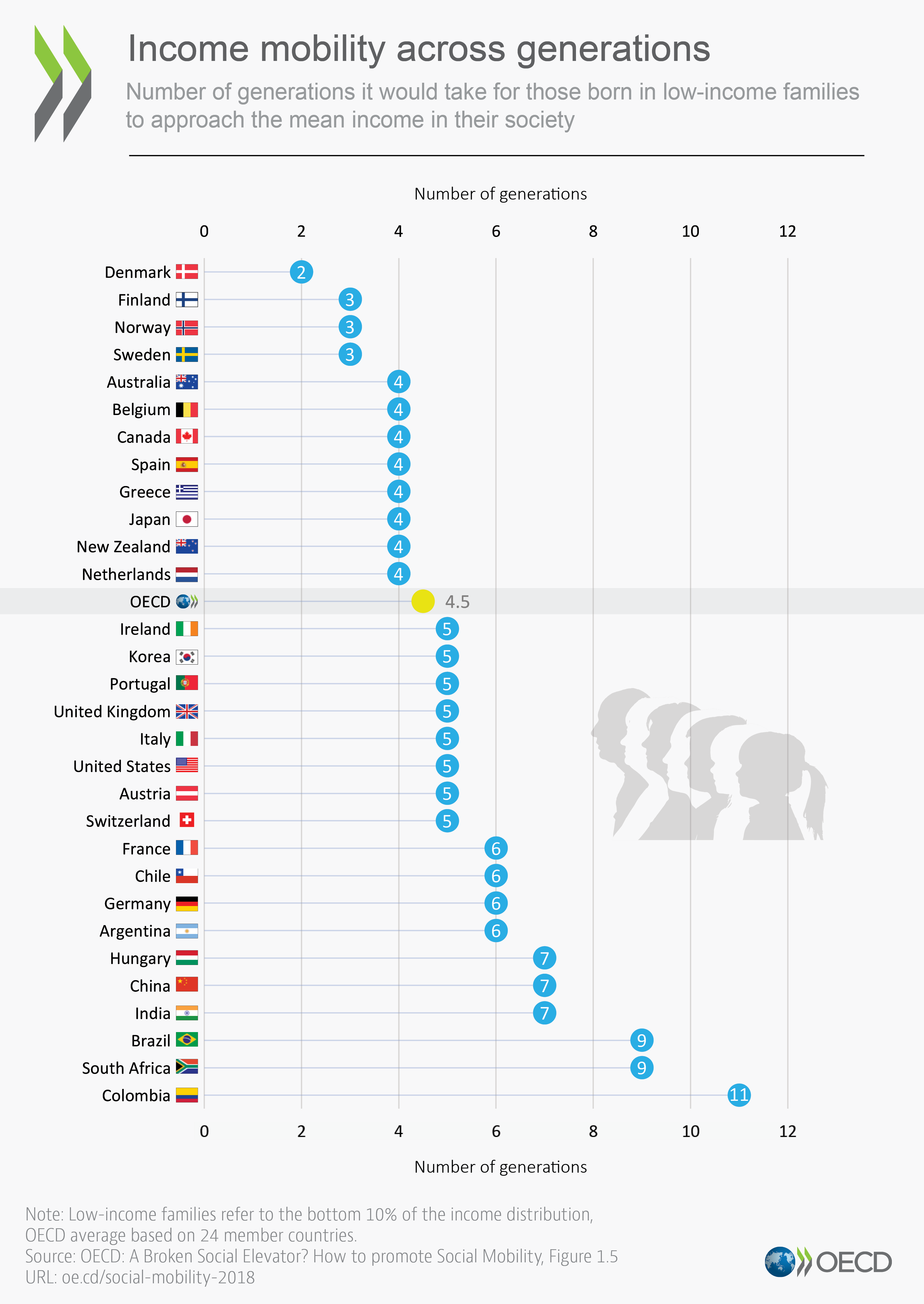

That OECD study is really tricky as it only goes to mean income. The interesting bit would be to really rich and there I am not sure Scandinavia would score so well.

Thank you for the chart. Germany is further down the list than even I thought, admittedly. How sad ist that. Here I thought that at least Germany having a good social safety net and free university would mean it is somewhat easy to pull yourself out of low income if you are intelligent and have the drive, as well as parents who gave you a bit of encouragement in your early years. Seems like even that is harder than I thought.

Do you have one for mean income to upper class by chance? Even +1 Std Deviation move would be significant in terms of wealth building.

I think traditionally most people in most countries ignored the stock market and consider it boring to talk about.

Maybe less so in the USA? Not sure.

But a lot of computer folks have spare money at the moment, and in that situation you have a few options: consume more, keep it in a savings account, or invest. And some significant proportion choose invest.

Keep it in a savings account is a common option, but quite a bad idea.

Probably the majority of people who invest do so in property, considering it safer than stocks (which I disagree with, although there are other reasons to like property).

This may be changing a bit in recent years, because access is easier now. In Sydney I see adverts for stock brokers at the bus station.

Seems like some gamblers have switched to the stock market to get their fix too.

In the US if you have a retirement savings account (which is very advantageous to have) it’s likely to be a 401k or IRA which you have to manage yourself. So having some basic understanding of the stock market is essential to your financial future.

You are likely indirectly into the stockmarket, through pension funds or social security. In the USA, a lot of people (especially in big tech) are more directly involved through a 401k, which allows to pick stock/bonds.

It could also be that you prioritize investing money into a house instead?

Ah don’t be afraid of it. You’re missing out an opportunity to live a worryless retirement and to even leave a solid chunk of assets to your kids/partner. Simply invest a few hundreds euros (probably 300-400 will be enough) every month into an ETF which tracks some of the very broad market indices like MSCI World, FTSE All World or even S&P500. You have very good chances of becoming a millionaire or almost-millionaire by the time you retire. Good luck!

My parents didn't do stock market, for the simple fact that you got a nice interest from a savings account. Those times are gone now. Some people have a hard time grasping the alternatives.

Stocks are considered "risky", but if you have a 10+ years timeframe, an index fund is not risky at all.

I also have 75% of acquaintances that don't do stock market or crypto. And that's the reason why my savings are outperforming all of them.

Also Europe here, and leaving aside what others have said about how everyone is invested in the stock market whether explicitly or not (which is entirely true), this rings true for me as well - it's also backed up by data.

This makes sense when you think about it - in the past you would have built habits and understanding from relatives and your community (e.g. "Don't invest in stocks that's gambling and they always crash!"), whereas since the Internet came along people have more access to data and perspectives from more places.

All of the above said, the last few years, and especially since the lockdowns, the behaviour in the markets has been really alarming. The FT.com link above touches on this, but the rush into [stocks/cryptocurrencies/leveraged funds/options] is something I've never seen before in my lifetime. I don't think the world has ever seen anything like this level of amplified speculation. Bitcoin, Leveraged ETFs, and Options didn't exist in the 1920's. The Netherlands had futures contracts towards the end of Tulipmania, but I haven't seen anything to say that they were leveraged.

In the late 1990's it was clear and readily apparent to everyone that the Internet was a massively important step forward. We agreed on that. It wasn't a controversial or widely disputed viewpoint. The market still imploded because of the sheer amount of rampant speculation, so to think something worse won't happen to a multi-trillion dollar market based on a technology many people think only has value for running Ponzi schemes seems to be pretty irrational.

To top it off, the wall of hype seems impenetrable at this stage ("have fun staying poor!" etc), so it remains to be seen what happens when the plates stop spinning this time.

tldr; Your grandparents might be proven right after all.

> In the late 1990's it was clear and readily apparent to everyone that the Internet was a massively important step forward. We agreed on that. It wasn't a controversial or widely disputed viewpoint. The market still imploded because of the sheer amount of rampant speculation, so to think something worse won't happen to a multi-trillion dollar market based on a technology many people think only has value for running Ponzi schemes seems to be pretty irrational.

In the 1990s it wasn't clear to everyone that the internet was a massively important step forward. You were younger and probably part of the technically-savvy, forward-looking generation that could clearly see the internet being massively important in future. However, *many* people in the older demographic lacked this insight and didn't fully embrace the internet until the mid to late 2000's. I think we'll see the same thing play out with crypto. Writing everything off in the sector as being ponzi is especially flippant.

Personally I have a philosophical (read marxist) reason to avoid it. Fundamentally I see the stock market as an exploitation tool which the rich use to siphon money away from workers and into their own pockets without contributing.

Every dollar you get but didn’t work for was a dollar that somebody else worked for but didn’t get. The stock market is full of transactions which yields profits for the rich while leaving workers at a loss by means of lower benefits. I refuse to participate and become a class traitor.

I’ve never worked in an industry which tries to push stocks onto you as much as software development. They keep paying me out options, giving me stock plans, etc. My strategy is to get sell as soon as I’m able, and transfer the money to a savings account in my local credit union. Don’t let them get away with not giving me my money, but don’t let them dictate how I keep my savings.

profits, outside of law encroachment or sheer luck are due to risk taken, the majority of adults dont want to risk more than their time and as we age our risk aversion increase. Creators of wealth are few and between, because they risk more and usually are more skilled than the average joe. This is also the reason why wealth dont survive over generations . these are few of the "marketing driven" meritocracy we have and taking part in this ecoomic competition is normal. morality arise when a public company has a dirty business model and one can decide to not support them, choosing ESG investments (real not marketed)

>This is also the reason why wealth dont survive over generations .

There is loads of counterexamples for this though. Especially in older countries in Europe it can become very apparent.

Also having wealth (trough inheritance) enables one both more opportunities and reduces risk.

A poor person taking a "gamble" on a business (if they can start one that doesn't require long rampup or capital) will struggle to feed themselves if it fails. A rich person (if not just focused on inherited assets) can try multiple times and is often encouraged to because of this but also trough exposure to fundamentals from family.

Isn't being offered stock in your own company broadly consistent with Marxist principles: workers own a share of the wealth they create? Maybe not as much of a share as they'd like, but I wouldn't have thought that was reason to avoid taking any.

Off-topic from the thrust of this conversation, but I always considered the above extremally risky. If your company goes tits-up, you loose your job and your savings.

This happened to a lot of people during the dot-com crash of 2000.

(Unless you have a high risk tolerance, you will want to diversify much more.)

It's orthogonal to Marxism but Marx and Engels both engaged in stock trading (not to mention that Engels literally owned a factory).

Employment is by definition exploitative because a capitalist system requires the owner to derive profits from labor, i.e. pay workers only a part of the value they generate. This isn't a value judgment, this is a matter of definitions: the capitalist mode of production is by definition exploitative because avoiding exploitation would steer the owner towards bankruptcy and thus kill the entire business.

The only solution to avoid this contradiction is to not have a separation between ownership and work, to abolish the capitalist class, i.e. ownership of a business is granted by working for that business, with all the rights and responsibilities ownership implies. However the ultimate ideological goal is usually (similar to how Free Software doesn't want to control copyright but abolish ownership of software) to abolish the notion of ownership or even businesses as distinct entities, much like discrete ownership of land was a nonsensical concept before enclosure (i.e. it was "your land" because you used it and the community was okay with you using it).

I think the most frequent misunderstanding of communism comes from trying to fabricate communist structures within capitalist power dynamics. Most of the prominent "communist experiments" had very little to do with actual communism because they were built around the assumption that they were building a foundation for communism to happen later rather than directly building communism in the here and now (hence the Eastern Bloc phrase "real socialism" as a euphemism for authoritarian governments with mandatory labor and limited democratic instruments, none of which is compatible with the definition of communism).

The thing most people seem to forget is that the goal of "abolishing the capitalist class" is to also abolish the working class as a subjugated dependent group because it is only a meaningful concept when contrasted with an owning class. The Soviet Union failed terribly at this by replacing the capitalist class with bureaucrats, effectively still maintaining a distinct working class and hoping he bureaucracy would magically "wither away" eventually while doing nothing to make that happen. They also tend to forget that the distinction between capitalist and worker is purely about ownership and there are many overlapping hierarchies of power, and owner vs worker is merely one of them (although one of the most important ones).

hnbad answered this much more thoroughly than I’m able. I would just like to add that in my experience stock options and grants has been an excellent way of pretending to pay me more then they actually pay. It feels like they are giving me a lot extra until you actually look at the numbers. And I bet a lot of workers get fooled by this. For me it feels like an exercise in cognitive dissonance, that is my employer is trying manufacture a cognitive dissonance in my brain which favors them.

Of course owning these stocks gives me nothing over their monitory value, so having them benefits me nothing over having an interest account with equal interest rate. So I just look at them as a bonus pay with additional headaches (moving money out of the stock market is harder then to cash in a normal check). And as while the power imbalance exists between workers and bosses, I would rather just get paid in regular salaries without the extra complexities.

In Iceland there is mandatory retirement funds. You can choose which fund and many people pick a fund that is only made off of government bonds. More people probably don’t have a clue what their retirement fund is made off, it is just some number on their paycheck, so they participate in the stock market both indirectly and unknowingly. I think it is kind of a stretch to say that these people are doing stocks. Most people I know use every opportunity to withdraw early from their fund.

At most these people do stocks like a person who returns their compost to the city does public gardening.

{kind=link}