It's a good counterpoint. Every developed country will end up as Japan eventually [1], and timing won't help you; where else would you put your investment assets to get exposure to similar risk adjusted returns (developing country returns expose you to greater risk)? Waiting for values to decline will be ineffective, as central banks will acquire assets to prop them up (Bank of Japan is the largest owner of the Nikkei [2]). Returns will decline, and the cost to obtain those declining returns will rapidly increase as trillions of fiat worth of capital chases it.

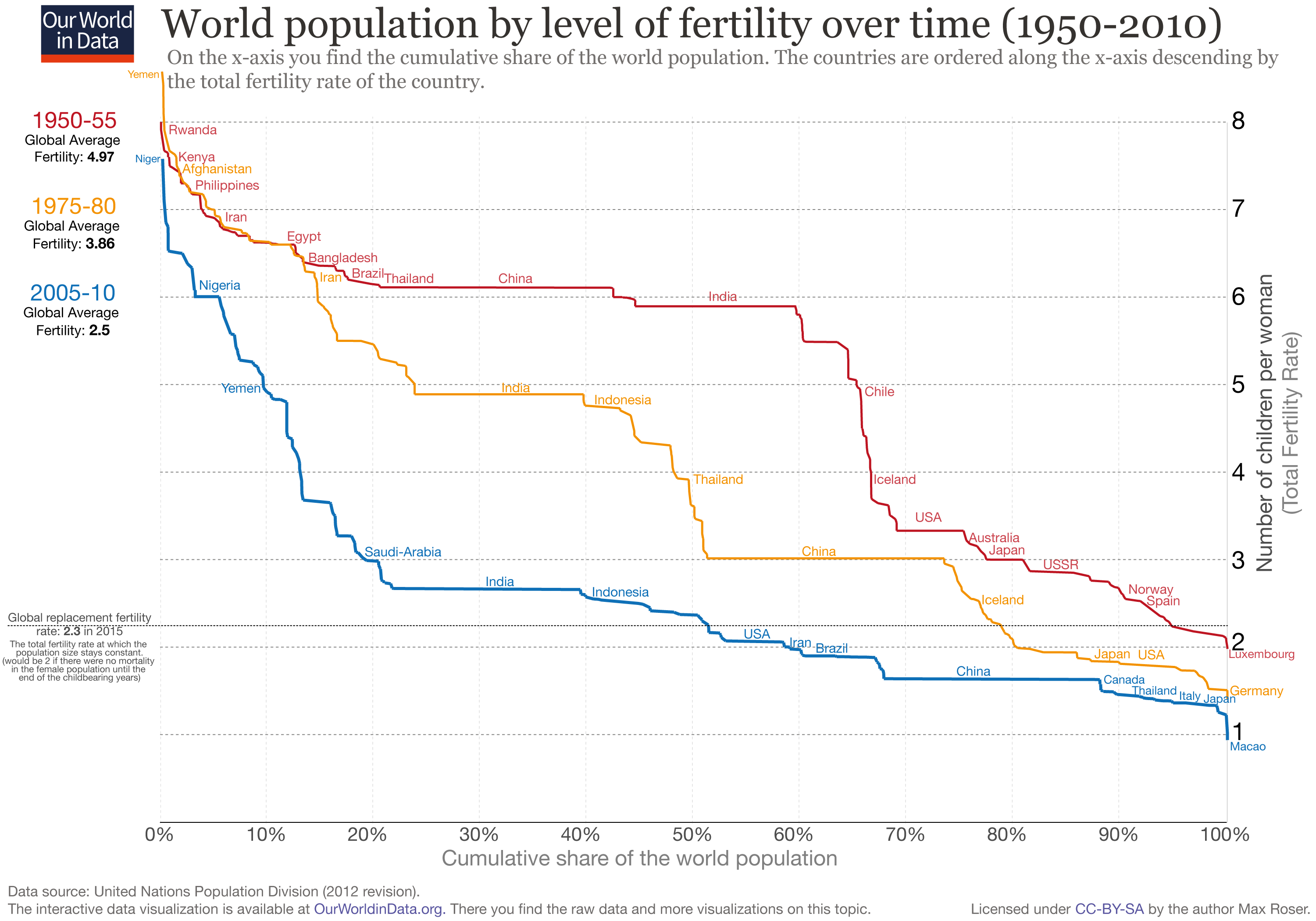

Over a long enough period, stonks only go up because that is what we've collectively agreed on, and government will backstop at all costs [2] while population and productivity extracted from that population declines over time [3].

I recommend "Shrinking-population Economics: Lessons From Japan" [3] on this topic.

Markets do seem to only go up, but the stocks on the market today are very different from 10, 20, 30+ years ago. I know that poorly performing stocks are eventually removed from indices and exchanges and they are replaced with new ones. Is it the case the market always going up in the long run is actually due to survivorship bias?

Say you confidently bought the roaring Eurostox 600 in March 2000.

You saw it coming back to its value in July 2007.

Then reach 1% gain in March 2015. And a 7% gain in Feb 2020.

Buying S&P, or the Apple, Amazon and Tesla ones is another story.

Looking at the average can be misleading.

FYI that's just closer to periodically investing. Dollar Cost averaging is more along the lines of "I already have $100 in my account and will invest $10/month for 10 months."

According to Investopedia: "A perfect example of dollar cost averaging is its use in 401(k) plans...an employee can select a pre-determined amount of their salary..."

Exactly. Look at the stock market from 1970 to today. 2001 and 2008 are a blip on the radar.

What this is missing is the amount of time investors are investing in. Day traders don’t care about tomorrow, they care about the difference between 9 am and 4 pm. Options traders might care about the next few weeks. If you are investing for 20+ years in a retirement account, you don’t care about the bubble. It will self correct over a year and by the time you withdraw, stocks are significantly up.

Bonds make sense if you are investing for 1 month to say 3 years.

It certainly didn't go nowhere. Obviously, if someone bought and sold their entire portfolio on those (VERY cherry-picked - just look at the graph, lol) days, they would have made 0 dollars.

But look on either side of that blip and there is plenty of profit.

{kind=link}

I'm not denying the existence of bubbles, busts, and crashes, but historically and on average, the stock market does only go up.

This market is overvalued and will likely correct, but that doesn't mean it won't continue to rise on the aggregate.